Life OS: Money — The 3-Lane Budget System

In a previous post, I explained why tracking your money matters.

Now I’m going to show you how mine is actually structured.

You can set this up in Monarch or any solid budgeting app. I reference Monarch throughout this series because it’s the one that works best for me. I’ll include my referral link at the end if you want to try it.

If you want to go deeper into money psychology and automation, I highly recommend reading I Will Teach You To Be Rich. It had a major impact on how I think about systems and spending. (I may get a commission if you decide to purchase the book)

Prefer to Listen?

If you’d rather listen to a walkthrough of this system instead of reading it, I recorded a beginner-friendly breakdown on The Average Ninja Podcast

Let’s begin.

The 3-Lane System

I organize my budget into three simple lanes:

Essentials

Guilt-Free Spending

Future

That’s it.

If your money doesn’t have lanes, it feels chaotic.

If it has lanes, it feels calm.

Here’s the important part:

Your percentages must fit inside your income.

If your Essentials are 85% of your income and you’re trying to invest 20%, that’s not discipline — that’s denial.

Percentages only work if they’re honest.

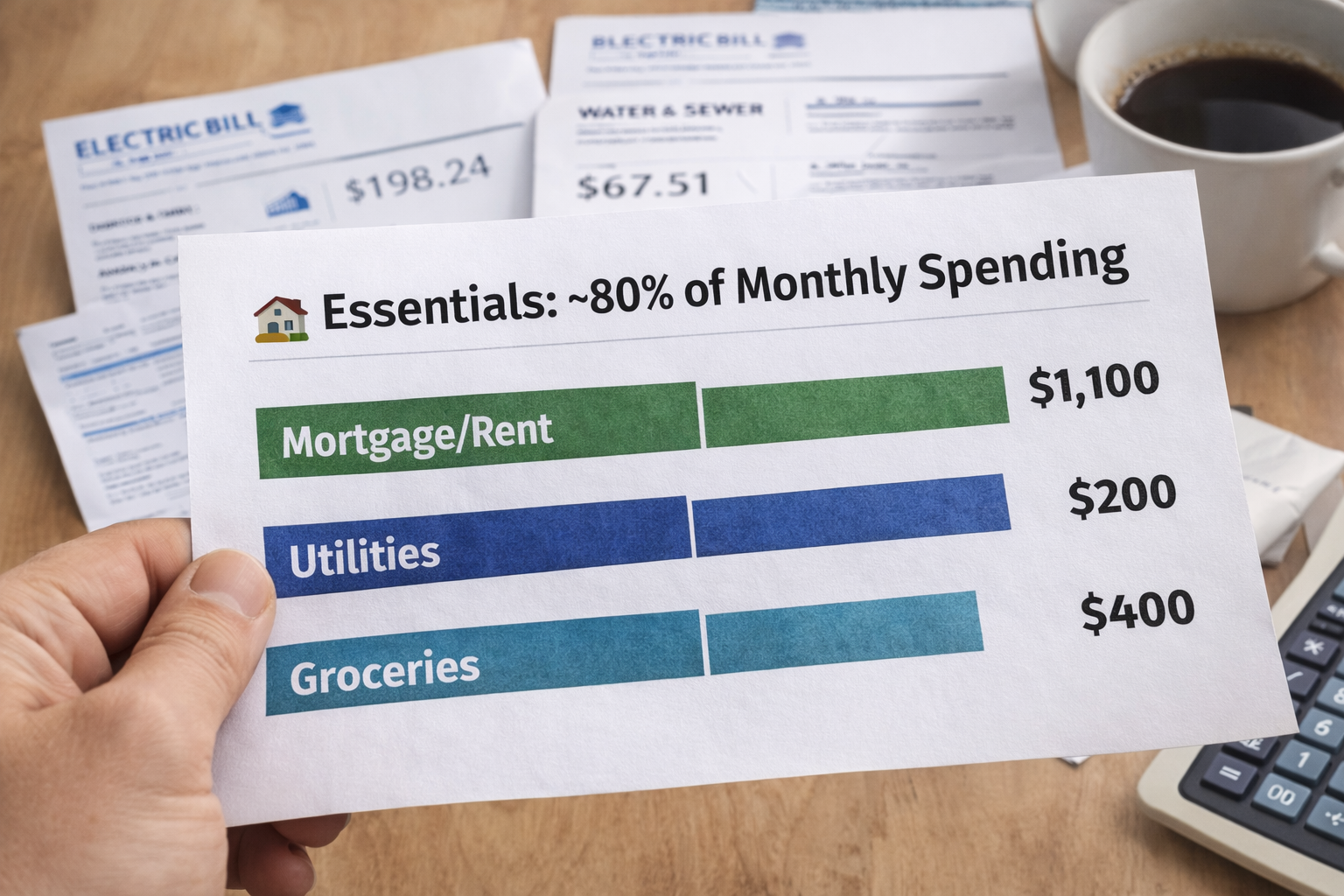

🏠 Essentials: ~80% of Monthly Spending

This includes:

Mortgage

Utilities

Groceries

Insurance

Gas & auto maintenance

HOA

Pets

Home improvement

This number matters more than income.

Because this tells me the baseline cost of being me.

And I’ll be honest — right now, my percentages are a little thin.

I recently purchased a house.

I invested in Karate RX’s drop ceiling.

I built out my home gym.

That increased my fixed costs.

So my margin isn’t huge right now.

And that’s okay.

Because I know it.

Most people feel financial pressure because they don’t know their margins. I feel pressure sometimes too — but it’s measured pressure.

There’s a difference.

🧠 Guilt-Free Spending: ~11–12%

This includes:

Supplements

Books

Apps & subscriptions

Therapy

Personal development

Occasional electronics

I live differently than most people I imagine.

I don’t enjoy going out much.

I don’t spend heavily on restaurants.

I don’t chase nightlife.

My life is simple:

I work out.

I teach karate.

I create content.

I play video games.

Video games are cheap entertainment compared to most lifestyles.

So my discretionary spending reflects that.

Your budget should reflect your values.

🚀 Future: ~8–10%

This is automated.

Wedding fund

Long-term savings

Investing

The rule is simple:

Never skip the transfer.

Even if it’s small.

Consistency beats ambition.

And again — it has to fit inside your income.

If your savings rate is forcing you into credit card debt, it’s not discipline.

It’s imbalance.

⏩ Automation Is The Backbone

I do not manually move money around every month.

I use scheduled bank transfers to:

Pay myself

Fund savings

Invest

It happens automatically.

If it requires willpower, it’s not a system.

Monarch also allows you to create “rules” that automatically categorize transactions. If a charge hits from a specific vendor, it gets sorted instantly.

That reduces friction.

The less friction, the more consistent you’ll be.

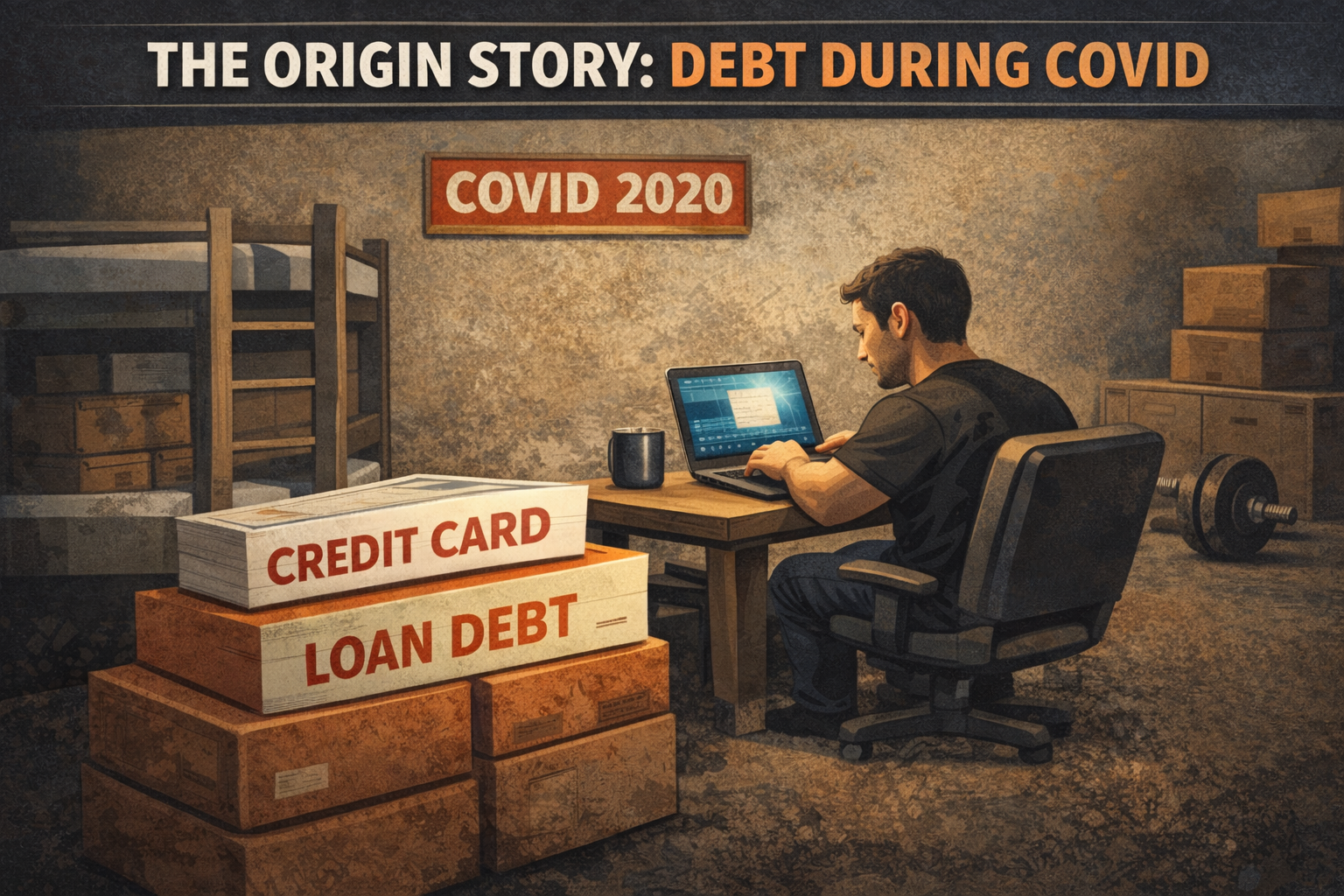

⚠️ The Origin Story: Debt During COVID

When COVID hit during year three of Karate RX, things were not comfortable.

I had loans.

I had credit card debt.

Revenue was uncertain.

That was my origin story phase.

I rented out two rooms in my townhome.

I built out my garage and lived there.

Not because it was glamorous.

Because it created margin.

Then I automated debt payments.

Every month, money moved automatically toward:

Loans

Credit cards

I didn’t negotiate with myself.

I shoveled money into debt reduction until it was gone.

That discipline cleared my debt and allowed me to begin investing.

That wasn’t motivation.

That was structure.

💵 Budgeting Through Expansion

This past year wasn’t quiet financially.

I:

Purchased a new house

Invested in upgrading the gym’s drop ceiling

Sold my old townhome

Built out my home gym

And now I’m rebuilding business reserves for taxes

That’s a lot of movement.

But here’s the important part:

None of it was chaotic.

It was sequenced.

The House

When I bought my new home, my Essentials percentage increased.

That’s expected.

Housing is the biggest lever in most people’s budgets.

But because I already knew my structure, I didn’t guess.

I recalculated.

That’s the difference between:

“I hope this works.”

And:

“I know what this costs.”

The Gym Ceiling Investment

The ceiling upgrade at the gym wasn’t an impulse decision.

It was a capital investment in the business.

The business runs on a two-account structure:

Checking → operations

Savings → taxes + operating reserve

Funds move automatically into savings.

When I chose to invest in the ceiling, I knew:

What the reserve target was

What would temporarily decrease

And how long it would take to rebuild

Now I’m rebuilding reserves intentionally.

No scrambling.

No panic at tax time.

That’s budgeting.

The Townhome Strategy (Years in the Making)

For years — not just when I was preparing to sell — I automated extra payments toward the mortgage on my old townhome.

When I had roommates, it was more aggressive. After Kash moved in and I wasn’t renting rooms, it lowered to just $50 per month.

Lower principal meant:

More equity.

More flexibility.

More optionality.

By the time I sold, that discipline had compounded.

That extra equity helped fund:

The transition into my new house

The home gym buildout

A smoother financial reset and lower mortgage on my new home

That wasn’t emotional.

It was structural.

🍂 Understanding Financial Seasons

Right now, I’m in what I call a:

Stability Rebuild Phase.

Travel is paused

Expansion is paused

Reserves are rebuilding

Taxes are prioritized

Budgeting isn’t static.

It has seasons.

Expansion.

Stabilization.

Optimization.

Rebuild.

If you don’t understand the season you’re in, you’ll make emotional decisions.

📅 The Weekly Ritual

Once a week, I:

Review my cash flow and budget

Let Monarch’s rules auto-categorize most transactions

Adjust anything that needs manual correction

Look at my percentages

No drama.

Systems are meant to be adjusted — not worshipped.

🤖 Using ChatGPT To Build Your Budget

If you want help setting this up inside your own life, here are useful prompts you can copy and paste into ChatGPT.

1️⃣ Find Your 3 Lanes

"Help me organize my monthly expenses into three categories: Essentials, Guilt-Free Spending, and Future. Here are my last 2–3 months of expenses: (paste them here)."

2️⃣ Calculate Honest Percentages

"Based on my total monthly income of $____ and my expenses listed below, calculate what percentage goes to Essentials, Lifestyle, and Savings. Tell me if this is sustainable."

3️⃣ Identify Margin Problems

"Looking at my budget, where is my margin thin? What category is putting the most pressure on my financial stability?"

4️⃣ Create an Automation Plan

"Design a simple automation system for my finances. I get paid on (dates). Help me schedule transfers for bills, savings, and investing so I don’t have to move money manually."

5️⃣ Debt Payoff Structure

"Create an automated debt payoff plan using my current balances and income. I want something sustainable, not aggressive, and I do not want to miss payments."

6️⃣ Financial Season Check

"Based on my current budget and goals, am I in an Expansion, Stabilization, Optimization, or Rebuild season? What should I prioritize right now?"

Use ChatGPT as a thinking partner — not a replacement for discipline.

It can help you design structure.

You still have to follow it.

💭 Final Thought

Budgeting isn’t about restriction.

It’s about clarity.

When you know your structure — even when it’s tight — you move differently.

You stop guessing.

You stop hoping.

You start sequencing.

Structure builds freedom.

If you want to try the budgeting app I use, here’s my Monarch referral link:

https://www.monarchmoney.com/referral/iitqvyu9zo

See you in the next Life OS: Money post.

~ Average Ninja